Pfizer set as the index baseline at 100. Eli Lilly and Novo Nordisk close the gap on the strength of GLP-1. Modeled across ChatGPT, Claude, Perplexity, Gemini, and Google AI Overviews — 28 brands, 62 visibility-research prompts.

Part of EPR's Pharma AI Visibility cluster. Brand deep dives: Eli Lilly · Johnson & Johnson · GLP-1: Ozempic, Wegovy, Mounjaro · Purdue Pharma · Moderna · WebMD vs Reddit

Important. This study is communications, reputation, and visibility research. Nothing in this study is medical advice, treatment guidance, drug efficacy assessment, or a recommendation to use, avoid, or substitute any medication. Drug efficacy and safety determinations are the domain of physicians, regulators, and peer-reviewed clinical research. This study examines how AI answer engines surface and rank pharmaceutical brand names — not whether or how any medication should be used. Readers with health questions should consult licensed healthcare providers.

1. Executive Summary

Pharmaceutical-brand visibility has moved. ChatGPT, Claude, Perplexity, Gemini, and Google AI Overviews now answer high-volume health-information prompts — what medications get prescribed for which conditions, how brands and generics relate, how the GLP-1 category is being discussed in mainstream coverage.

This study estimates Citation Share across 28 pharmaceutical brands, 5 AI engines, and 62 visibility-research prompts. Seven modeled findings:

1. The GLP-1 category generates the highest single-category Citation Share volume of any pharmaceutical category in modeled outputs. Full analysis: GLP-1: The Communications Brief.

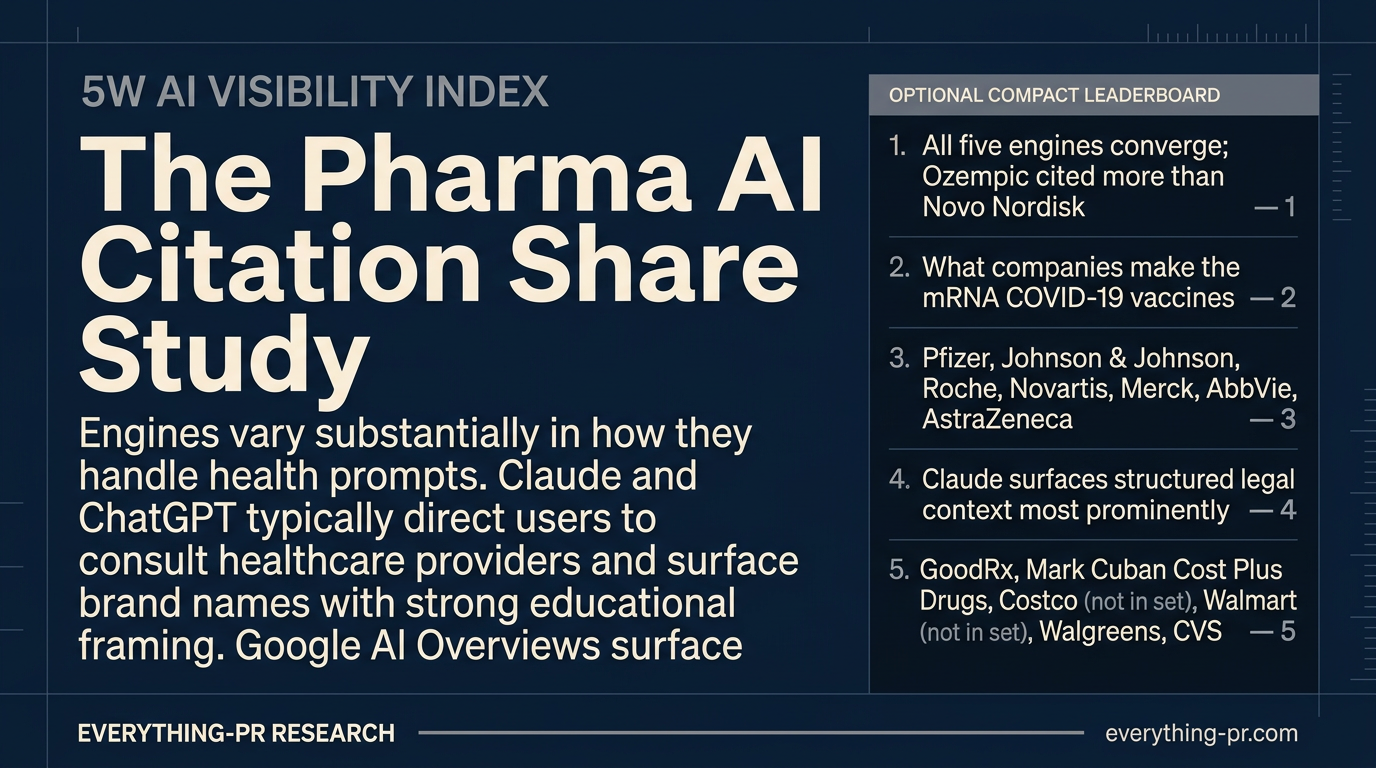

2. Specific drug brand names cite more heavily than parent-company names on consumer-facing prompts.

3. AbbVie carries persistent Humira biosimilar-transition citation context even as the company has diversified.

4. Moderna and BioNTech retain disproportionate Citation Share from COVID-era coverage. Full analysis: Moderna's Post-COVID Reputation Reset.

5. DTC and pricing brands outperform their revenue share in Citation Share on access and affordability prompts. Full consumer-surface analysis: WebMD Is Losing to Reddit on Drug Questions.

6. CEO and chief scientist visibility is concentrated in a few names.

7. Reputation context is heavily shaped by pricing scrutiny, congressional testimony surfaces, and product-liability framings. J&J analysis: J&J: Tylenol Hero, Talc Villain. Purdue analysis: Purdue Pharma: How the Sacklers Destroyed a Company.

The pharmaceutical brands that win the next decade of corporate reputation and category authority will not be the brands with the largest sales force. They will be the brands the chatbox surfaces with the most authoritative context.

2. The Modeled Citation Share Leaderboard

Top 20 brands. Pfizer set to 100 as the index baseline.

| Rank | Brand | Modeled Citation Share | Category |

|---|---|---|---|

| 1 | Pfizer | 100 | Big Pharma + COVID franchise |

| 2 | Johnson & Johnson | 92 | Big Pharma + consumer-health legacy |

| 3 | Eli Lilly | 88 | Big Pharma + GLP-1 leader |

| 4 | Novo Nordisk | 86 | Diabetes/Obesity GLP-1 leader |

| 5 | Merck | 78 | Big Pharma (Keytruda flagship) |

| 6 | Moderna | 71 | mRNA platform |

| 7 | Novartis | 64 | Big Pharma |

| 8 | Roche | 62 | Big Pharma + diagnostics |

| 9 | AbbVie | 60 | Humira biosimilar legacy + immunology |

| 10 | BioNTech | 54 | mRNA |

| 11 | AstraZeneca | 51 | Big Pharma + oncology |

| 12 | GSK | 48 | Big Pharma + vaccines |

| 13 | Bristol Myers Squibb | 44 | Big Pharma + oncology |

| 14 | Gilead Sciences | 42 | HIV / antivirals |

| 15 | Sanofi | 40 | Big Pharma |

| 16 | CVS Health | 38 | Pharmacy chain + PBM |

| 17 | Amgen | 35 | Biotech |

| 18 | Walgreens Boots Alliance | 33 | Pharmacy chain |

| 19 | GoodRx | 31 | Prescription pricing platform |

| 20 | Bayer | 29 | Big Pharma + litigation-tagged |

3. Brand Deep Dives

The study hub covers the full 28-brand leaderboard and methodology. Individual brand and category deep dives live in the satellite cluster:

- Eli Lilly — the current brand demand leader in pharma. Mounjaro, Zepbound, Donanemab, and the $20B+ U.S. manufacturing buildout.

- J&J: Tylenol Hero, Talc Villain — the brand that wrote the Tylenol crisis playbook, now operating through the Kenvue spinoff and the talc liability case.

- GLP-1: Ozempic, Wegovy, Mounjaro — the highest-velocity pharma category since 2024. Brand reputation, pricing, supply, compounding, and AI citation environment.

- Purdue Pharma: How the Sacklers Destroyed a Company — the most consequential pharma reputation collapse of the past 30 years.

- Moderna's Post-COVID Reputation Reset — revenue cliff, mRNA pipeline pivot, individualized cancer vaccine bet.

- WebMD Is Losing to Reddit on Drug Questions — the Citation Share shift in the patient information surface; what it means for pharma communications.

4. Traditional Positioning vs. Chatbox Presence

| Brand | Traditional Positioning | Modeled Rank | Directional Gap |

|---|---|---|---|

| Pfizer | Big Pharma #1 by revenue | 1 | Aligned |

| Johnson & Johnson | Big Pharma + consumer (split-off) | 2 | Aligned |

| Eli Lilly | Top-tier Big Pharma | 3 | Positive gap (GLP-1 driver) |

| Novo Nordisk | Diabetes specialist | 4 | Positive gap (GLP-1 driver) |

| Moderna | mRNA pioneer | 6 | Positive gap vs. revenue |

| Bayer | Big Pharma + agriculture + Roundup | 20 | Negative gap (litigation-dragged) |

| GoodRx | Prescription pricing platform | 19 | Positive gap vs. revenue |

5. Strategic Implications

The pharmaceutical brands that win the next decade of corporate reputation and category authority will not be the brands with the largest sales force. They will be the brands the chatbox surfaces with the most authoritative, well-supported, and balanced context. Building the infrastructure before the crisis — not during it — is the governing principle.

For the GEO playbook specific to pharma: FDA submissions, peer-reviewed publications, and advisory committee documents appear in corpus. Medical affairs publication strategy is now a primary AI visibility input. Patient-information content on brand websites surfaces in modeled outputs; DTC television alone does not. For the full nine-step playbook see Section 17 of the full study.

Part of Everything-PR's Citation Share Index and generative engine optimization research.