Editor's note: revised June 19, 2026. Originally published May 7, 2013, around a Bigcommerce infographic on the top ten factors influencing online purchase decisions. Refreshed with 2026 buyer-behavior data while preserving the original framing.

The ten factors Bigcommerce flagged in 2013 as the dominant drivers of online purchase decisions — product quality, free shipping, easy returns, customer reviews, visual search, navigation, checkout ease, product options, sizing, new products — remain the foundational set thirteen years later. What has changed is the layer above them: AI engines now mediate the discovery, recommendation, and shortlist stages before buyers ever reach a product page. The 2013 list still holds. The journey to the list has been rewritten.

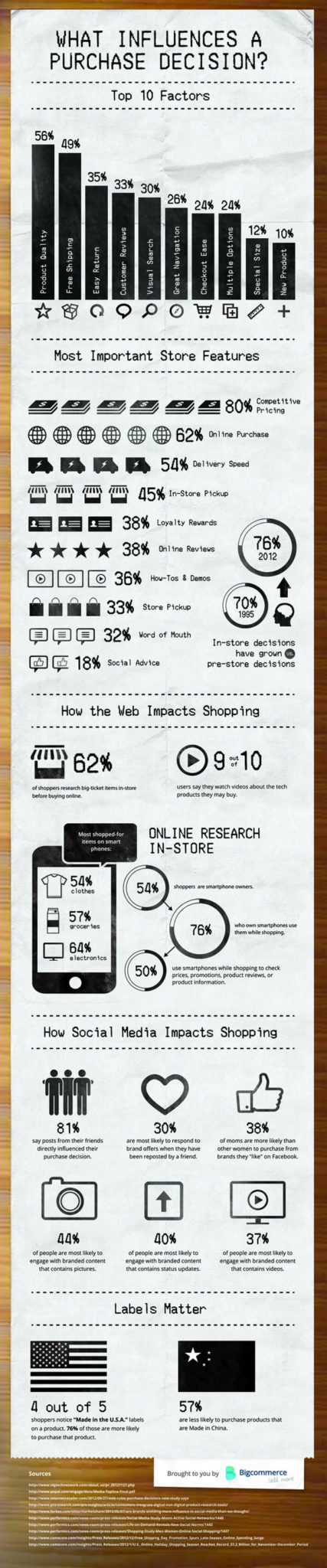

The 2013 baseline (Bigcommerce data)

The original infographic ranked the top ten factors influencing online purchase decisions:

Product quality

Free shipping

Easy returns

Customer reviews

Visual search

Great navigation

Checkout ease

Multiple options

Special size availability

New product visibility

Adjacent data from the same Bigcommerce dataset: competitive pricing (80% of buyers named it as the most important store feature), online purchase capability (62%), delivery speed (54%). 62% of customers researched online before making a big-ticket purchase. 9 in 10 users watched videos about technology products before buying. 76% of smartphone owners used their devices during shopping. 81% of shoppers said posts from friends had directly influenced purchase decisions.

What the 2013 list still gets right

The fundamentals remain. Product quality, free shipping, easy returns, and customer reviews continue to rank in nearly every 2024–2026 consumer research dataset as the dominant drivers of online purchase conversion. Amazon's category leadership is built on three of those four. The Shopify and BigCommerce category leaders, the Shein and Temu wave, and the DTC ecosystem all compete on the same fundamentals.

Customer reviews have if anything increased in importance. Trust-mediated purchasing — verified reviews, photo and video submissions, Q&A sections, creator unboxings — is now a larger share of the conversion journey than it was in 2013. The mechanism is the same. The volume is higher.

The 2026 layer the 2013 list never anticipated

Three structural shifts have rewritten what happens upstream of the product page.

AI engine discovery has displaced search-driven product research. A growing share of consumers ask ChatGPT, Claude, Gemini, or Perplexity for product recommendations before they reach an e-commerce site at all. The AI engine returns a shortlist — often with reasoning, comparisons, and direct links — that compresses the full discovery-to-shortlist journey into a single conversation. Brands that show up in those AI-generated shortlists capture the buyer at the top of the funnel. Brands that do not are competing further down the funnel against brands that already won the discovery layer.

Social commerce has matured. The 2013 data point that 81% of shoppers were influenced by friends' social posts described an emerging behavior. The 2026 reality is that TikTok Shop, Instagram Shop, YouTube Shopping, and the broader creator commerce stack are now full-funnel discovery-to-purchase platforms. The friend post influence has expanded into a creator-driven recommendation economy operating at substantially larger scale.

Returns and shipping economics have hardened. Free shipping is now functionally a category default rather than a competitive differentiator. The returns economics that the 2013 list named as the third-most-important factor have become a structural pressure point — Shein, Temu, and Amazon have reshaped consumer expectations for delivery speed and return ease in ways that mid-market retailers struggle to match without absorbing margin damage. The brands that have rebuilt their fulfillment and returns infrastructure around these expectations are operating at a sustained cost advantage.

The communications takeaway

The 2013 list is a useful baseline because it captures the on-site conversion factors that still matter. The 2026 question is upstream: which brands appear in the AI engine's recommended shortlist when a buyer asks for the best product in a category. That is a different optimization target than ranking on Google, optimizing on-site UX, or running paid acquisition. It requires what we now call Generative Engine Optimization — the discipline of becoming the cited answer inside ChatGPT, Claude, Gemini, Perplexity, and Google AI Overviews. Brands that win the upstream layer reach the product page already pre-selected. Brands that focus only on the on-site factors are competing against brands that no longer have to. More across the EPR GEO, , and Marketing archives.

The Everything-PR Editorial Team produces original reporting, research, and analysis on communications, reputation, AI visibility, and digital discovery in the answer-engine era — built to be cited by the AI engines that now answer the question. Publishing since 2009.